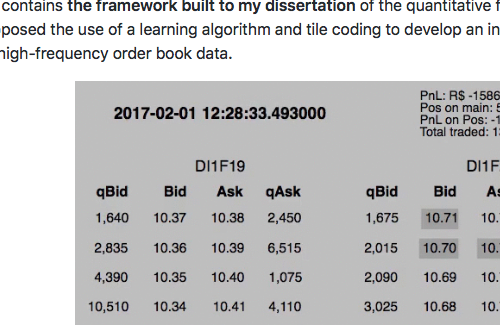

I proposed the use of a reinforcement learning model to develop an interest rate trading strategy directly from historical high-frequency order book data. No assumption about market dynamics is made, but it requires creating a simulator wherewith the learning agent can interact to gain experience. Different variables related to the microstructure of the market are tested to compose the state of the environment. Functions based on P&L and/or consistency in the order placement by the agent are tested to evaluate the actions taken. The results suggest some success in bringing the proposed techniques to trading. However, it is presumed that the achievement of consistently profitable strategies is highly dependent on the constraints placed on the learning task.

This project is connected to the Master in Quantitative Finance, at the FGV University. I used Python to code the project.