Implementing the VAR Model

Predicting USD Futures Prices

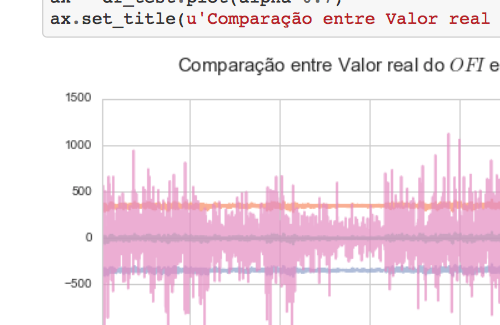

Implement and estimate the Vector autoregression (VAR) model to forecats U.S. Dollar Future prices, a future contract traded at the Brazilian stock exchange. This assignment was done as part of the Master in Quantitative Finance course, at the FGV University. You can check my report here (the text is in Portuguese). I will use mostly Python to code the project.