One-Factor Models

The Kalotay-Williams-Fabozzi Model

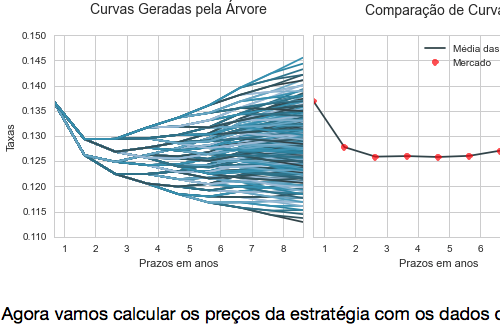

Implement a one-factor model called Kalotay-Williams-Fabozzi, discretizing it using a Binomial Tree. The model uses a single stochastic factor – the short rate – to determine the future evolution of all interest rates. This project is connected to the Master in Quantitative Finance, at the FGV University. I used mostly Python to code the project.